.png)

The way pensions are treated for Inheritance Tax is changing in a big way. From April 2027, pension funds and death benefits will be included in your estate for IHT purposes.

In this blog, I’ll run through why this is happening, how it may affect you and your beneficiaries, and what you can do to plan in the meantime.

What is the current pensions and IHT position?

The existing rules, which apply until April 2027, mean that the majority of unused pension funds and death benefits aren’t counted as part of your taxable estate.

Defined contribution (DC) pension schemes usually operate under a discretionary trust structure. In other words, the pension isn’t owned outright at death, so HMRC doesn’t factor it into Inheritance Tax.

This has made pensions one of the most effective ways to transfer wealth in a tax-efficient way. But that is changing.

Will pensions be included in Inheritance Tax?

Yes, from 6 April 2027, most unused pension funds and death benefits will be included in your estate for IHT purposes. This is a major change with significant implications for a lot of pension holders.

In fact, this is probably the biggest reform affecting pensions and IHT in years, and fundamentally changes how we need to think about retirement and estate planning.

What is changing in April 2027?

- Pension funds and death benefits will be treated as part of your estate when calculating IHT.

- This applies regardless of whether the scheme has discretion or not.

- Death in service benefits from registered pension schemes are excluded.

The existing spouse/civil partner and charity exemptions continue to apply, however, so funds passing to these beneficiaries can remain tax-free.

Why is IHT changing for pensions?

This is a highly controversial reform, and there are vocal opponents and defenders of the new legislation. The government’s rationale is that pensions should be used for retirement income, not as tax vehicles. They saw pensions as an IHT loophole, being used to transfer wealth without tax.

From an adviser’s perspective, there may be some significant consequences of this change, including greater complexity for families, very high effective tax rates (pensions could face 40% IHT plus income tax when beneficiaries withdraw funds), and distorted behaviour among pensions savers.

How will this affect your pension and IHT position?

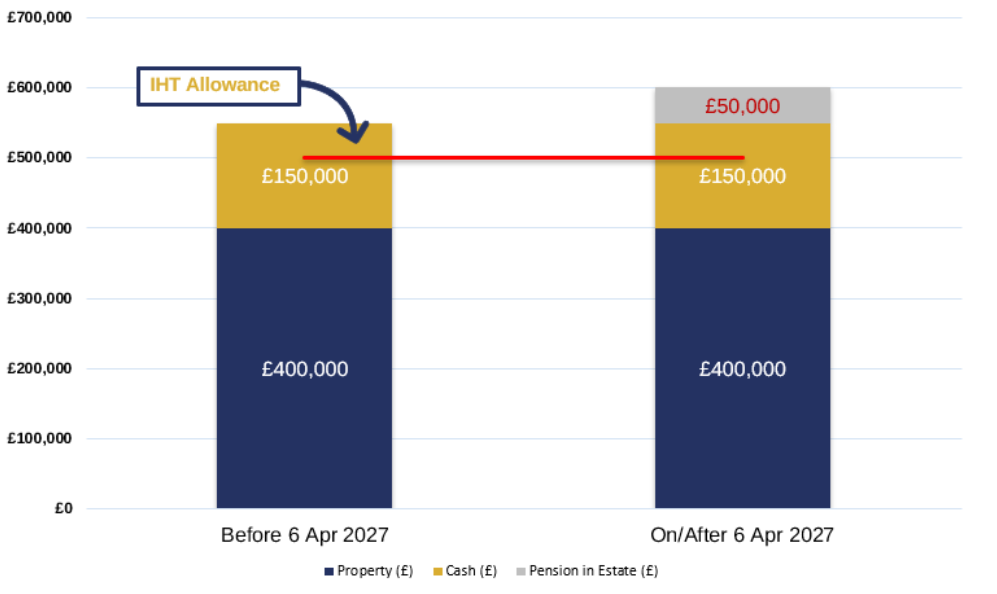

Example Scenario

The following tables and chart show an example of how including pension assets in an your estate from 6 April 2027 could increase the inheritance tax (IHT) liability under the assumed scenario. In this example, the IHT bill would be £20,000 higher.

Example: Impact of Pension Inclusion on Inheritance Tax

What can you do to prepare?

Regardless of your age and current position, if you are likely to be impacted by these changes, the time to start planning is now. Here are some key points to consider for 2026/27.

- Review your beneficiary nominations so that pensions paid to the people you choose (such as your spouse) are still tax free.

- Check whether drawing down some pension before death could help; however, it’s important to remember withdrawals can trigger an income tax bill.

- Revisit your will and estate planning to align with the new tax treatment

Speak to a qualified adviser about whether gifts, trusts, life assurance or charitable giving can help you meet your goals.

.jpg)

%2010.jpg)

.webp)

.svg)