.png)

For limited companies in the UK, the CT600 form is one of the key documents of a company’s Corporation Tax return. It is the principal document that you must use to tell HM Revenue and Customs (HMRC) about your company finances and calculate the amount of tax that is owed. In this blog, we’ll outline the key features of this all-important document.

Please note: This blog outlines the key sections of the CT600 form that are likely to be a factor for most companies. It is not exhaustive, and there are other sections of relevance to companies with more niche circumstances.

What is the CT600?

The CT600 is the official form that UK companies use to report their annual profits, losses, and tax liabilities to HMRC. This comprehensive document serves as your company's formal declaration of its financial position and determines how much corporation tax your business owes for the accounting period (if applicable).

It is not the whole Corporation Tax return; the CT600 is just one component of a completed return submitted to HMRC. The full return includes the following documents and reports:

- The CT600 form

- The company’s statutory annual accounts (or financial statements)

- Tax computations that support the figures that appear on the CT600

- Any other supplementary pages that are required

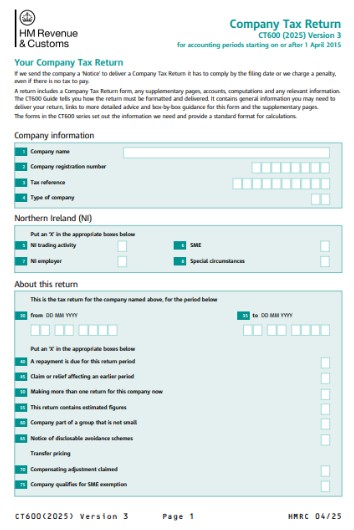

What is included in the CT600 form?

The CT600 can be a lengthy and complex form, depending upon the complexity of the company it is being completed for. The CT600 form is comprehensive and designed to capture all the relevant financial data HMRC needs.

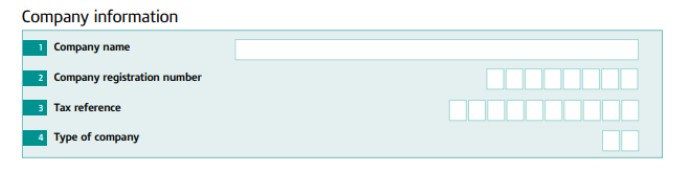

Details on the company and its accounting period

Firstly, the CT600 requests information on your company’s name, registration number, and Unique Taxpayer Reference (UTR). In addition to this info, companies will also need to specify which accounting period the Corporation Tax (CT) return covers. It’s worth noting here that no accounting period for corporation tax can exceed 12 months. Finally, any special circumstances will need to be declared too, such as if you are due a repayment.

Company income and profits

The form then needs to know how much money the company made during the accounting period; this means:

- Trading profits or losses

- Other income, such as bank interest or rent

- Any chargeable gains or allowable losses

- Information on any Coronavirus support schemes and payments received

Corporation Tax deductions and reliefs

You will then have an opportunity to reduce your company’s taxable profits to ensure you are only paying what you are legally required to. This includes both deductions and reliefs, including the following:

- Trading losses

- Capital allowances for things like equipment purchases

- Costs incurred in running the business

- Qualifying charitable donations

- Tax credits, such as R&D tax reliefs

- Double taxation relief, if the company has been taxed on income in another jurisdiction

Tax Calculations

Using the information already included, the CT600 then guides companies through how to calculate total profits before any deductions, applying any applicable marginal or other reliefs, and finally arriving at the taxable profits figure.

This is then used to calculate the actual Corporation Tax amount that is due based on the rates that apply to your company. At this point it’s crucial to consider the number of associated companies as this will affect the corporation tax rates applicable to your company.

Payments and Repayments

This section details any Corporation Tax payments you've already made for the period. If you've overpaid, it will show the repayment due and includes space for your bank details for a direct refund.

Declaration

The CT600 requires a formal declaration from the person submitting the return, confirming that the information provided is accurate and complete to the best of their knowledge.

Supplementary CT600 pages

Depending on the specific activities of the company, additional supplementary pages may need to be submitted alongside the CT600. These tend to cover niche areas that don’t apply to the majority of companies. Three of the most common supplementary pages are:

- CT600A: Used for loans to company directors

- CT600C: Used for corporate group and consortium relief claims

- CT600L: Used for Research & Development (R&D) tax relief claims

The importance of tax reconciliation

The CT600 form and accounts detail the financial and tax position of the company, and tax reconciliation is an important step in connecting your accounting profits to your taxable profits.

In other words, your financial accounts aim to give a “true and fair view” of the company’s performance and are prepared under strict accounting standards (like FRS 102 and FRS 105).

Tax computations, however, adjust the accounting profits to comply with HMRC’s rules. The reconciliation process ensures that tax liability declared in the CT600 is derived accurately from accounting records, with a clear audit trail.

Making Tax Digital for Corporation Tax

Making Tax Digital is currently fully in force for VAT, and the government is in the process of rolling it out for Income Tax via Self Assessment (ITSA). It was generally understood that Corporation Tax would follow in due course. However, in July 2025, HMRC decided not to proceed with Making Tax Digital for Corporation Tax. Had this extension of MTD moved forward as originally planned, companies would have been obligated to maintain digital records using software and submit quarterly income and expense updates to HMRC.

Naturally, Gravitate will be happy to help you with all your Corporation Tax needs.

CT600 FAQs

Can I file my own CT600?

You can file your own CT600 (Company Tax Return) without hiring an accountant, however it's very important you have sufficient understanding of your business finances and how Corporation Tax works. Filing yourself is most common for small companies with straightforward affairs. But remember you are legally responsible for ensuring the data is accurate. If your company has complex transactions, R&D claims, or international trade, professional advice is a really good idea to avoid costly errors or HMRC penalties.

Can I amend a CT600?

You can amend a CT600 if you discover an error after submission. HMRC allows you to make changes to a filed return within 12 months of the filing deadline. To amend it, you must resubmit the entire return, including any corrected accounts or computations, and mark it clearly as an "amended" return. If the deadline has passed, you may need to write to HMRC directly to claim Overpayment Relief or disclose a voluntary correction.

Can I submit CT600 online?

Online submission is actually the mandatory method for almost all UK limited companies. Paper filings are only accepted in very rare circumstances, such as for companies with a "reasonable excuse" or those filing in Welsh.

Can I file CT600 without software?

From 1 April 2026, almost all companies will be required to use commercial software to file their CT600 and accounts

.jpg)

%2010.jpg)

.webp)

.svg)